Resource Market Insights – February 2026

2026 COMMODITY BOOM: GOLD, COPPER AND THE CASE FOR CANADIAN RESOURCE INVESTORS

What a start to 2026!

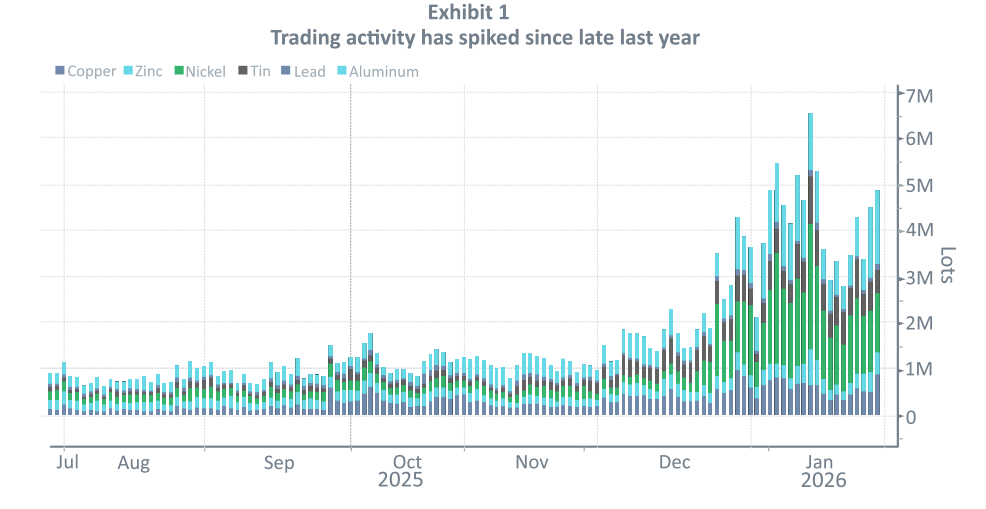

Despite recent market fluctuations, 2026 has kicked off with a strong performance in the metals and mining sector, driven by a surge in global demand and speculative interest. Over the past month, China’s trading activity has surged, with record volumes moving through the Shanghai Futures Exchange, signaling increasing market momentum (see Exhibit 1).

Source: Bloomberg, Shanghai Futures Exchange

Source: Bloomberg, Shanghai Futures Exchange

Year-to-date, gold has risen over 13%, marking its strongest start to a year in decades, despite a recent pullback from its all-time highs. Silver has climbed 19%, and while copper’s rise has been more moderate, it has still gained more than 9% (based on recent highs), marking the largest percentage increase since 2009. Aluminum has also seen significant buying activity, with institutional investors growing increasingly optimistic about copper and aluminum, which has driven prices to record highs. This boost in demand has extended to the London Metal Exchange (LME), creating even more price strength. Even lithium and rare earth elements, typically secondary commodities, have had a strong start to the year. With precious metals hitting new highs and industrial metals like copper and aluminum seeing unparalleled activity, the first quarter of 2026 is shaping up to be a standout one for metals and mining investors.

But what’s behind this market surge? How do we make sense of these remarkable gains, and more importantly, what do they mean for investors in the Canadian resource sector, particularly within the flow-through space?

GOLD: The Asset of Stability in Unstable Times

Let’s begin with gold, which has shown significant growth. What’s driving this surge, and can we expect it to continue? The answer lies in a mix of factors, including geopolitical tensions, inflation concerns, and central bank behavior.

Geopolitical Instability Fuels Gold’s Safe-Haven Appeal.

The U.S. policy landscape has been marked by a series of unpredictable moves, creating geopolitical risks that have investors seeking safe-haven assets like gold. From government shutdowns to military escalations in the Middle East, tensions are rising, particularly with Iran. Additionally, U.S. actions in Venezuela—including the controversial capture of President Maduro—have further heightened global instability. Moreover, President Trump’s moves to assert control over Greenland—citing national security concerns over Russia and China—have raised tensions not just in Greenland, but across Europe. Trade wars, along with aggressive rhetoric toward countries like Cuba, Colombia, and Mexico, have also contributed to a heightened sense of uncertainty. As geopolitical risks rise, gold has remained a top safe-haven asset, attracting investors seeking stability amidst this uncertainty.

Central Banks and ETFs: The Rising Forces Behind Gold Demand. Gold’s price rally is also strongly supported by sustained demand from Exchange-Traded Funds (ETFs) and central banks. Year-to-date, ETFs have purchased 1.4 million ounces of gold, valued at $876.1 million. This brings total gold held by ETFs to 100.4 million ounces, a 1.4% increase in 2026 so far. The largest ETF in the precious metals space, SPDR Gold Shares, holds 35 million ounces, valued at $162.9 billion.

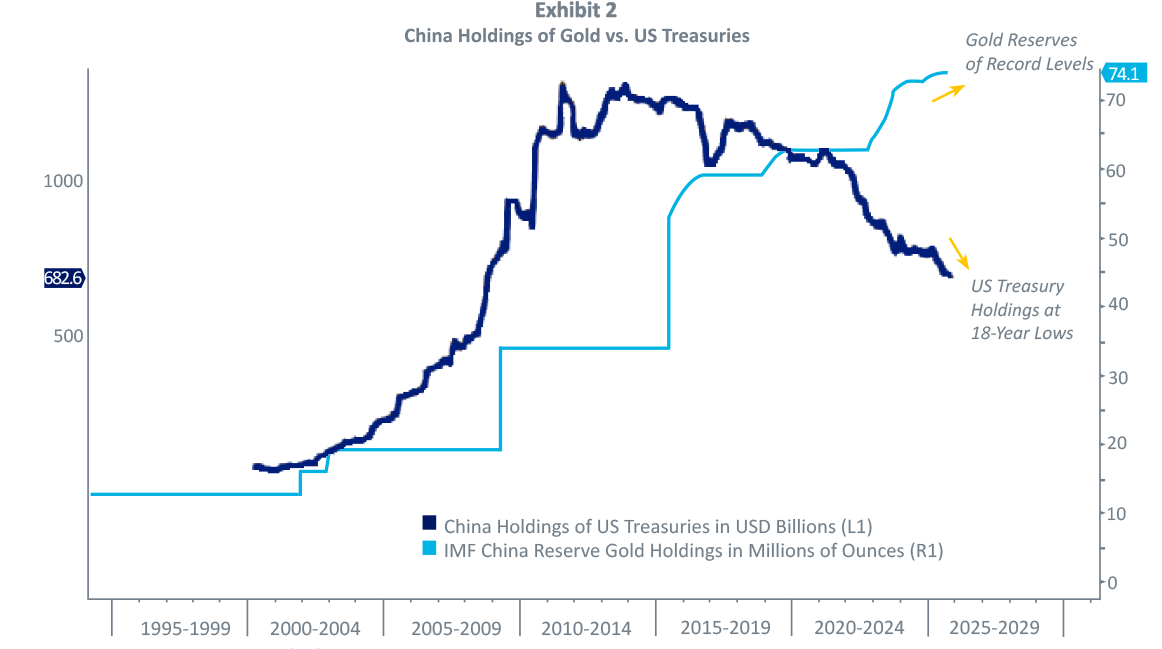

Simultaneously, central banks have also been aggressively increasing their gold reserves. As of 2025, for the first time since 1996, foreign central banks collectively held more gold than U.S. Treasuries in their reserves. (See China’s holdings of gold vs. US Treasuries in Exhibit 2). Emerging markets like China, India, and Turkey have been at the forefront of this gold accumulation, as part of a broader strategy to reduce reliance on the U.S. dollar due to its diminishing value and rising geopolitical risks.

Source: Bloomberg, Chart as of 1/20/2026

Source: Bloomberg, Chart as of 1/20/2026

This shift away from U.S. debt in favor of gold is a pivotal development, signaling a long-term rebalancing of global reserves and supporting the price of gold in the process. The growing demand for gold by both private investors and central banks is expected to continue pushing prices higher in the medium to long term.

U.S. Dollar Weakness. In addition to the geopolitical instability, the U.S. dollar continues to lose its appeal on the global stage. The Bloomberg DXY Index shows a 3% drop in the dollar in January 2026 alone, exacerbated by President Trump’s trade policies, including his largest import levies on foreign goods. The dollar’s continued weakness signals heightened global volatility, during which real assets—especially gold—tend to outperform. Gold’s role as an effective hedge against currency fluctuations becomes increasingly apparent during periods of dollar weakness.

Bitcoin: Not a Safe-Haven Yet. In contrast, bitcoin has failed to emerge as a true safe-haven asset. Though it has gained attention as “digital gold,” bitcoin’s value has recently plummeted to levels last seen in April 2025 (around $73,000 per coin). Bitcoin’s volatile nature makes it more of a speculative play rather than a reliable store of value. During periods of heightened uncertainty and geopolitical unrest, gold continues to reign as the preferred safe-haven asset, while bitcoin remains a high-risk investment, especially in times of global market turmoil.

Gold Price Forecast and Outlook

As we move through 2026, the momentum behind gold shows no signs of slowing. JPMorgan’s forecast suggests that gold could reach between $8,000–$8,500 per ounce, driven by increased demand from both private investors and central banks. This would represent an additional 40% upside from current levels. Despite the recent market pullbacks, the long-term outlook remains strong, underpinned by ongoing global uncertainties and a potential further weakening of the dollar. The World Gold Council also projects a 15%–30% increase in gold prices over the next few years, as geopolitical tensions and concerns about the dollar’s stability continue to drive demand for gold.

COPPER: Tight Supply Meets Shifting Chinese Demand

In the case of copper, global supply remains tight, and this has been a major driver behind copper’s recent surge. Prices have risen by over 5% year-to-date, and the metal recently hit record highs of $14,500 per metric ton. The surge has been largely driven by speculative interest in China, combined with a long-term outlook fueled by constrained supply and strong demand for applications in electric vehicles, renewable energy, and data centers.

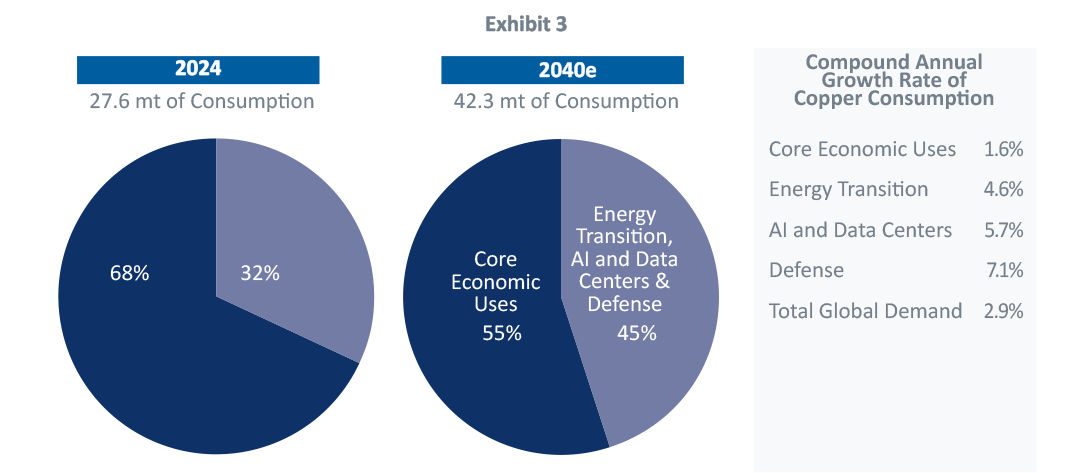

However, near-term signals from China have been more mixed. As copper prices have risen, the metal has become more expensive for fabricators in the world’s largest consuming nation, leading to a softening in spot market demand. This has caused inventories to rise in nation, leading to a softening in spot market demand. This has caused inventories to rise in London Metal Exchange (LME) warehouses across Asia. At the same time, Chinese copper output is expected to increase by 5% in 2026, after a 10% rise in 2025, as local smelters ramp up capacity. Despite these near-term fluctuations, copper prices are expected to remain supported by strong long-term fundamentals. Standard & Poor’s projects global copper consumption to grow by 50% by 2040, driven by increased demand for technology, defense spending, and the global energy transition (See Exhibit 3). Even with periodic dips in demand from China, copper’s long-term outlook remains highly positive.

Source: S&P Global, January,2026

The Marquest Advantage: Positioned for What’s Next

After a period of underperformance compared to large-cap mining stocks, junior miners are now showing strong momentum. The surge in commodity prices, combined with improved liquidity in the junior mining space, has boosted performance across the sector. This shift comes at a time when major mining companies are facing shortages of critical minerals such as base metals, uranium, and other key resources. This shortage has made junior miners prime targets for acquisition.

The strong demand for these resources, coupled with limited supply, presents a unique opportunity for junior miners, particularly those that are well-positioned to benefit from the ongoing commodity boom. For Marquest Flow-Through Limited Partnerships, this is an ideal time to gain exposure to junior mining companies with significant upside potential. In addition, the flow-through structure offers significant tax-efficient benefits, making these investments even more attractive.

With geopolitical tensions, currency fluctuations, and strong demand for base and precious metals, junior miners could benefit from both organic growth and the increasing likelihood of mergers and acquisitions. For investors, this could be the right time to tap into the growing metals and mining sector and capitalize on opportunities in the Canadian flow-through space.

Glenn G. Drodge, CFA

Senior Portfolio Manager