Resource Market Insights – March 2025

Gold’s Resurgence: Safe Haven in a Volatile 2025

First Quarter Market Update: Key Geopolitical Themes Shaping 2025

Three Drivers of Recent Volatility

As we enter 2025, market volatility is once again a major concern, with a chaotic, reckless, and disorganized White House driving much of the movement in equity markets. It appears the Trump administration almost thrives on turmoil (though perhaps almost is too generous). Many of Trump’s statements on tariff policy are incoherent and nonsensical, providing little clarity for those with even a basic understanding of economics and international trade. For market professionals managing investments, predicting what a volatile leader will do next regarding policy is nearly impossible. A prime example of this unpredictable behaviour occurred the morning of March 7, 2025, when Trump announced he was pausing tariffs to help Canada and Mexico. However, he also mentioned that tariffs could increase in the future, continuing to sow daily confusion.

Another ongoing risk is Trump’s erratic foreign policy, particularly after his recent calls with Putin and a shouting match with President Zelensky of Ukraine. Trump seems to have all but surrendered to Putin, with any peace terms appearing to be tailored to the Kremlin’s interests. By cozying up to Putin and sidelining Ukraine, Trump emboldens Russian aggression, which in turn strains U.S. alliances. While markets may perceive this as reducing geopolitical risk, the situation is far more complicated. Ukrainians will continue to resist Russian occupation, and any peace agreement with Russia remains highly questionable, given its history of supporting separatists following the 2014 war. Russia’s resources are stretched thin due to the war, and Trump’s approach provides Putin with a lifeline, increasing the risk of future Russian aggression. Ukrainians, who were betrayed by the West in 1994 when they gave up nuclear weapons in exchange for security assurances, will likely never trust the U.S. again. Historically, U.S. military interventions have left conflicts unresolved (e.g., Afghanistan, Iraq, Vietnam), and this pattern could repeat with Russia, destabilizing the global order.

Finally, China’s economic slowdown introduces another layer of uncertainty, particularly affecting the mining sector due to reduced demand and a below-consensus outlook for many companies. The Chinese economy is struggling due to a combination of internal and external factors, including a slowdown in key sectors like real estate, manufacturing, and exports. The real estate market is facing major defaults, and efforts to reduce debt have dampened growth. Meanwhile, an aging population and declining birth rates are limiting the labour force, while weak consumer confidence, lingering COVID-19 controls, and trade tensions with the U.S. further hinder recovery. Additionally, regulatory crackdowns on tech and private industries have created an uncertain business environment. Rising energy costs and global inflationary pressures are also challenges. These factors make it increasingly difficult for China to maintain its previous high growth rates. Moreover, the Trump administration’s threat of tariffs on Canadian, Mexican, and Chinese goods—potentially prompting retaliation from other nations—will undoubtedly impact Chinese economic growth. While North America consumes a relatively small portion of most metals (less than 10% of global copper, for example), the larger concern lies in the potential impact on Chinese consumption (which accounts for approximately 55% of global copper demand).

Commodities in Focus

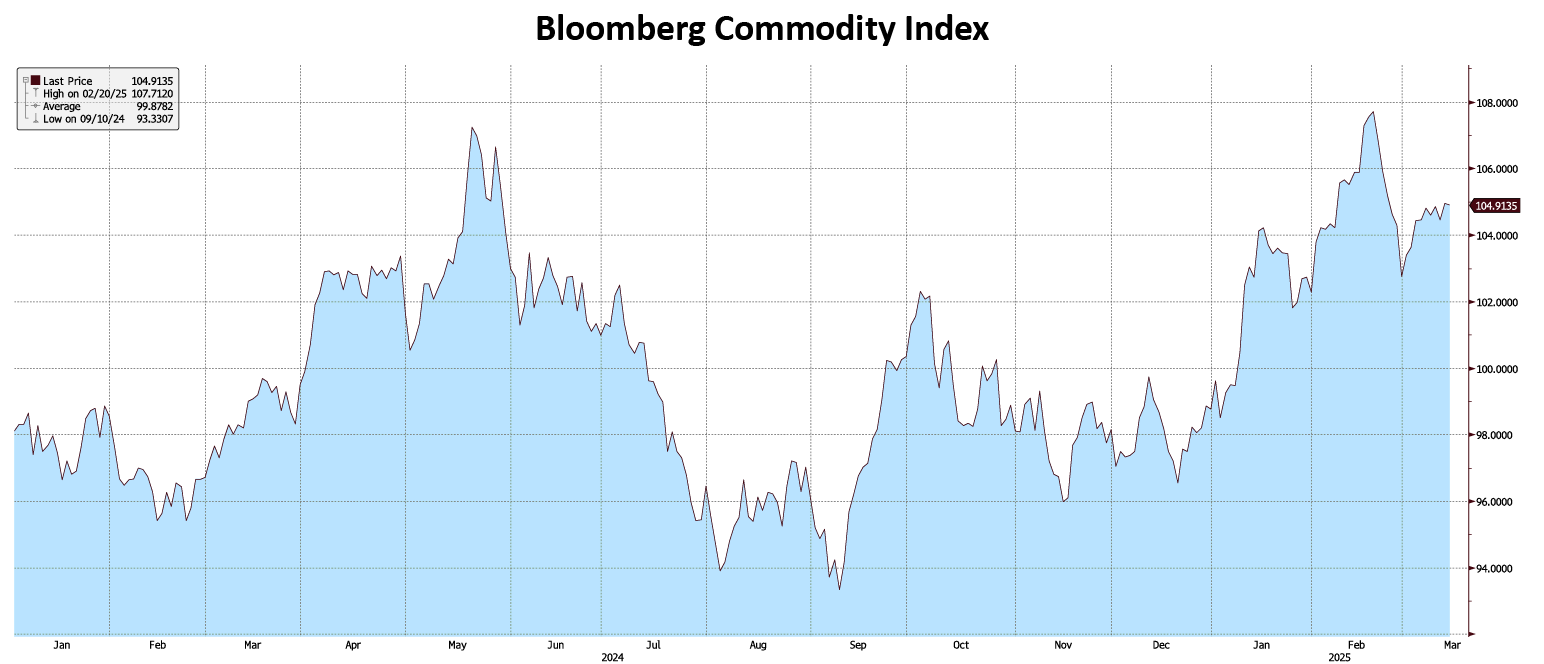

Given the key market risks at play, the Metals & Mining sector benefited from commodity prices remaining largely rangebound throughout most of 2024, with gains seen in 2025, as illustrated in the chart below. Likewise, base metal prices have remained within a stable range in recent weeks, despite risk-off sentiment driven by potential U.S. tariffs, geopolitical uncertainty, and the economic impact of weaker Chinese demand. This relative price stability has provided some support to the sector.

Source: Bloomberg

Gold has recently surpassed $3,000 USD per ounce, marking a new all-time high. Its performance over the past

year has been exceptional, driven by four key factors influencing its price:

- Inflation and the U.S. dollar

- Safe-haven demand

- Interest rates

- Central bank reserves and gold buying

Inflation and the US Dollar

Gold is widely regarded as a hedge against inflation. When inflation rises, the purchasing power of fiat currencies, such as the U.S. dollar, diminishes. In response, investors often turn to gold as a store of value to safeguard their wealth. As inflation rises and the U.S. dollar weakens, gold becomes more appealing to international buyers, driving its price higher.

As shown below, the U.S. dollar (white line) has depreciated significantly against other currencies in 2025, aligning with a rise in gold prices (gold line), as anticipated. We expect this trend to persist amid continued market turbulence driven by Donald Trump’s efforts to “punish” Canada, Mexico, Europe, and China over what he perceives— unjustly—as unfair trade practices.

Source: Bloomberg

Safe-Haven Asset

Gold is commonly viewed as a safe-haven asset during periods of geopolitical instability or economic turmoil. Events such as conflicts, wars, and financial crises (e.g., the 2008 financial crisis) often prompt investors to seek gold as a means of preserving wealth, driving its price higher. Given the ongoing geopolitical risks, we do not expect them to subside in the near term, further bolstering gold’s upward momentum.

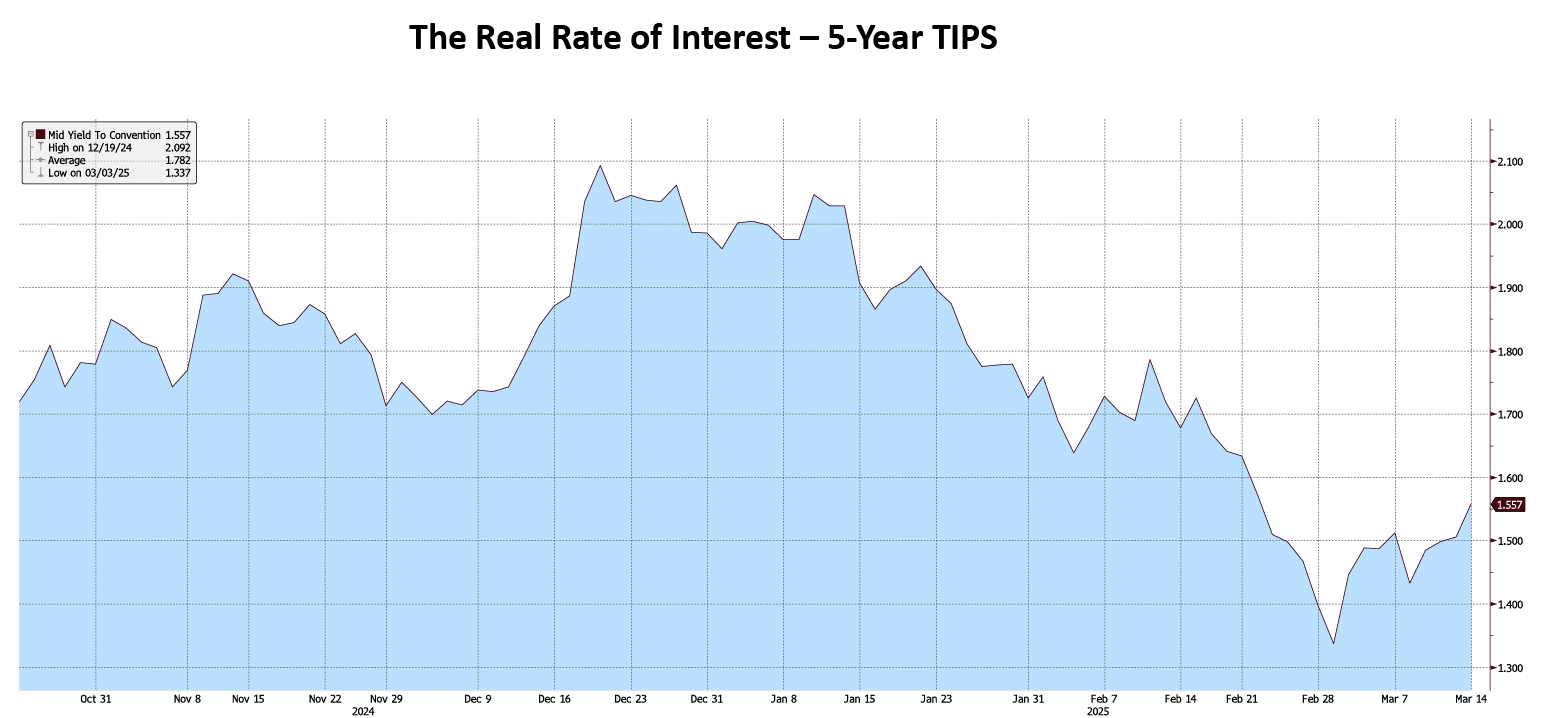

Interest Rates

Gold does not generate interest or dividends, making it less appealing when real interest rates (adjusted for inflation) rise, as investors can earn better returns from interest-bearing assets like bonds or savings accounts. Consequently, higher real interest rates often put downward pressure on gold prices, while lower real rates tend to boost demand for gold. As shown below, real interest rates have been declining since late last year.

Source: Bloomberg

Central Bank Reserves and Gold Buying

Central banks worldwide hold substantial gold reserves, and their buying or selling activity can significantly influence gold prices. In 2025, central banks have been net buyers of gold, with emerging market nations— particularly China, Uzbekistan, and Kazakhstan—leading the way. Poland and India have also continued to expand their reserves, adding to their holdings in both January and February of this year.

Why is this trend most pronounced in emerging markets? When the U.S. froze Russian assets through sanctions in 2022, other emerging economies took notice, realizing they could face similar risks. As a result, increasing gold reserves became a strategic move to safeguard their balance sheets. Additionally, central banks are accumulating gold as a hedge against inflation—just like many investors. With trade tensions and tariff wars fueling inflationary pressures, central banks are likely to continue purchasing physical gold, especially if global trade conflicts persist or escalate.

Summary

As we enter 2025, market volatility remains a significant concern, driven largely by the unpredictable behavior of the U.S. government under Trump, his erratic foreign policy, and China’s economic slowdown. However, these factors have supported gold, reinforcing its role as a safe-haven asset. Despite broader market instability, the Metals & Mining sector has remained relatively stable, benefiting from resilient commodity prices and steady demand. Gold has surged in value, driven by inflation, U.S. dollar depreciation, geopolitical instability, and declining real interest

rates. Additionally, central banks—especially in emerging markets—have continued accumulating gold reserves as a hedge against inflation and economic uncertainty. In light of these dynamics, Marquest Asset Management continues to overweight gold names and remains highly supportive of junior mining companies with strong gold projects seeking to raise funds in the flow-through space.

Glenn G. Drodge, CFA Senior Portfolio Manager